Thailand was not a developed country in the past, it was one of the poorest republics in the world. This happened because of the suppression of world-leading countries and ethnic conflicts in the motherland by the Thai people, But after the late 90s, it showed a significant step of growth. According to written records of The World Bank Group ;

“Thailand’s economy grew at an average annual rate of 7.5% in the boom years of 1960-1996”

But how did this chain of changes happen in this island country? What factors and lessons should other countries observe from their growth pattern?

Sit back and relax because by reaching the finishing line of this article you will learn everything about this transformation

Let the show begin!

Fintech

Creating any sort of tech boom will require more financial inclusion. After all, you need a critical mass of the population to buy into the tech economy, and it is hard to do this when people are financially excluded.

Thailand has gotten around this issue by supporting the fintech space. This, in turn, has led to the creation of neo banks, open banking, and other initiatives that ensure people can access the financial services they require.

With this access, they can participate in the tech economy, buy products and services, and drive the impressive growth we see today.

Embracing Novel Technologies

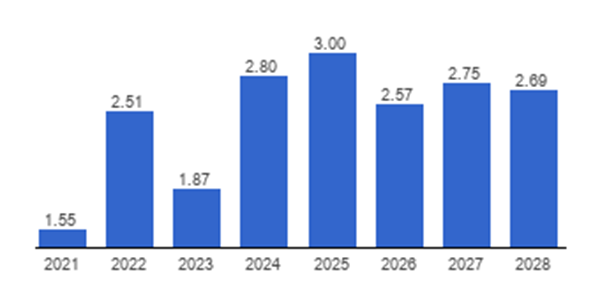

The graph presented here shows the expected rate of growth of Thailand’s economy by 2028.

The West has been heavily criticized for its treatment of novel technologies like blockchain. While embracing these technologies comes with some level of risk, Thailand has struck a balance between protecting users and encouraging the blockchain sector. Just look at the many wins the Thai crypto sector has seen, especially in the release of new tokens. Meme coins have especially been having a moment, with many successful presales and ICOs. As Somchai Wang writes, Cryptonews Thailand is full of stories of meme coin launches that have broken records and broken boundaries. And thanks to regulations like the Digital Asset Businesses Decree of 2024, consumers feel safe buying into these initiatives.

Data Centers

If we’re talking about tech booms, you have to acknowledge the ways that AI use has exploded in the last few years. From Chat-GPT answering basic questions to AI being used to create art and everything in between. As many of us will know, AI needs data centers to operate and a great number of them are located in Thailand. As of this article, the country is home to 42 centers, with many more underway and billions to be poured into this endeavor. Besides the immediate financial benefit, it positions the country as a vital city for AI development, ensuring its relevance in the industry for decades to come.

Foreign Investment

A major priority for the Thai government has been bringing in more foreign investment. This, of course, is dependent on creating a welcoming regular environment and has been achieved through the implementation of Thailand 4.0. This initiative is designed to turn the country into a high-tech space and has attracted a wealth of global tech giants to set up shop or partner with local companies. The increased presence of tech companies and support from the government has inevitably boosted its home-grown industry.

Did you know? Bangkok is called the Venice of the East because there are 83 canals. As many as 10,000 boats full of fruits, vegetables, and fish crowd the canals and create a floating market. (National Geographic Kids)

Widespread 5G

Just like with financial inclusion via fintech, Thailand has also made strides in creating digital access inclusion via 5G. A whopping 80% of the country has access to 5G connectivity, and download speeds are some of the most impressive in the world. At the end of the day, a tech boom is not just about a lot of products and services being put out but a mass of consumers able to access them as well. 5G has ensured that the Thai public may enjoy the fruits of this tech boom and that businesses in the country can compete with others around the world.

Tech-Driven Manufacturing

A big chunk of Thailand’s income comes from its manufacturing industry, and this has only gotten bigger with the tech boom. Internet of Things, blockchain technology, AI, and other tech innovations are being applied to the manufacturing process, which increases productivity and makes Thailand a bigger force in the global space. With all of this considered, the West is then faced with the challenge of pushing forward its manufacturing sector, both in terms of labor and tech innovations, if it will be able to compete.

Conclusion

In a few years, Thailand has established itself as one of the top forces in the tech sector. Much of this can be put down to deliberate effort by its government to increase both financial and digital inclusion, thus creating a landscape where tech innovation can thrive. By supporting the local industry and encouraging foreign businesses to get involved, this progress was made even faster. As several tech innovations like blockchain and AI continue to grow, their reliance on the Thai market means that this growth will continue for years to come.